Korea’s Fulfillment Startups Are Not the Next ShipBob or Deliverr

Why Naver’s fulfillment network, Coupang’s integrated logistics, and Korea’s compressed geography make the Korean fulfillment market structurally different from the U.S.

The Misleading Analogy: “Korea’s Deliverr”

Before analyzing Korea’s fulfillment startups, it’s worth revisiting how one of the most important companies in this space—Deliverr—was originally understood.

In 2018, 8VC wrote the following when they invested in Deliverr:

“The fulfillment industry is broken with fragmented segments and no integration across verticals… merchants, warehouses and carriers all suffer through inefficiencies because no one is orchestrating demand and supply.”

“Amazon is the only organization that has tackled this problem head on… all freight, 3PL, and shipping decisions employ end-to-end data analysis.”

“The industry is begging for a player that can orchestrate logistics between all three segments.”— Alex Kolicich, Partner at 8VC

(Source: https://medium.com/8vc/why-we-invested-in-deliverr)

Deliverr was not simply “a company connecting 3PL warehouses.”

It was built as a coordination layer for a fragmented fulfillment ecosystem outside of Amazon.

That distinction is the entire point.

In the U.S., e-commerce fulfillment outside Amazon was deeply disjointed:

Shopify merchants

Walmart sellers

eBay sellers

Independent D2C brands

3PL warehouses

Carrier networks

All operating in isolation.

Deliverr’s thesis was simple.

If you orchestrate inventory placement, warehouse selection, and carrier choice across this fragmented system, you can replicate Amazon-grade fulfillment without owning the infrastructure.

More importantly, Deliverr wasn’t solving for cost.

It was increasing revenue.

By enabling fast-shipping badges on marketplaces like Walmart and eBay, it directly improved seller conversion rates and sales velocity.

Fulfillment became a revenue driver, not just a cost center.

Deliverr should not be treated as the perfect fulfillment success story. Shopify acquired it for $2.1 billion in 2022, but Shopify later exited most of its logistics business and transferred Shopify Logistics, including Deliverr, to Flexport in 2023. That makes Deliverr important not because it proved the final operating model, but because it became the reference case every fulfillment startup could point to when explaining why an asset-light coordination layer might be valuable.

Why This Analogy Breaks in Korea

The problem is that many observers try to map this model directly onto Korea.

They ask:

“Which Korean company will become the next Deliverr?”

This is the wrong question.

Because Korea does not have the same structural gap.

In the U.S., Deliverr emerged because Amazon dominated one side of the market, and everything outside of Amazon remained fragmented.

In Korea, the structure is fundamentally different.

The market has already bifurcated into two dominant models:

Coupang → vertically integrated fulfillment

Naver → distributed fulfillment (NFA)

Coupang controls:

Consumer traffic

Inventory

Fulfillment centers

Delivery network

Returns experience

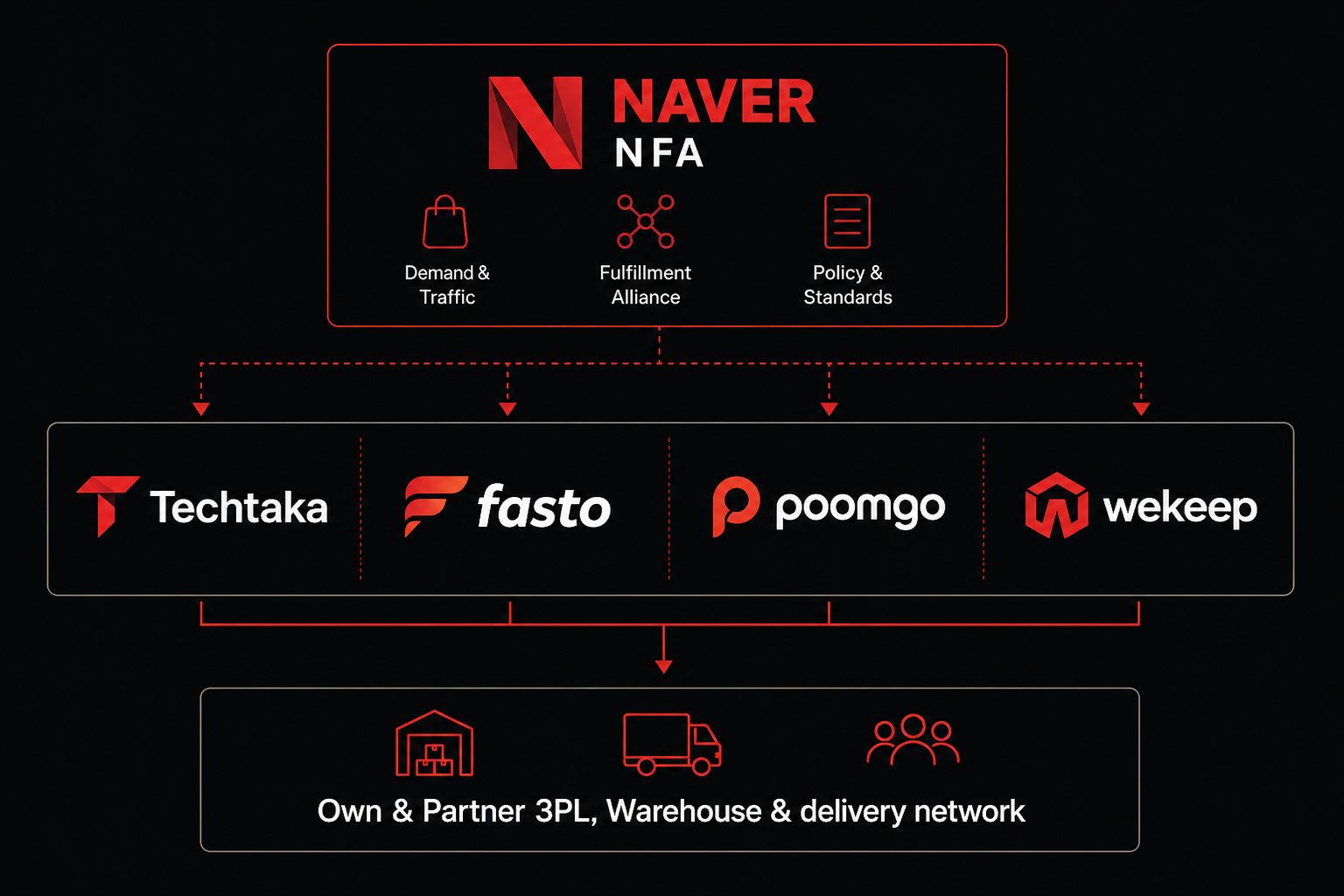

Naver, on the other hand, chose not to vertically integrate.

Instead, it built NFA (Naver Fulfillment Alliance)—a system that organizes external 3PLs into its ecosystem.

The position Deliverr tried to occupy in the U.S.—the orchestration layer between merchants, warehouses, and delivery networks—is already partially occupied in Korea by Naver. Naver may not operate like Deliverr, but it controls the ecosystem logic through NFA: traffic, seller access, fulfillment policy, and partner coordination.

That changes everything.

The Key Question

When evaluating companies like TechTaka, Fasto, Poomgo, or Wekeep, the question is not about funding, growth, or number of warehouses.

It is much simpler.

Without Naver, why would merchants choose this company?

If the answer is unclear, the company does not control demand.

And if it does not control demand, it is not a platform.

It is an execution layer.

This is where language becomes misleading.

Saying “we provide volume” implies platform power.

But in many cases, what is happening is different:

Platform generates demand (Naver) → Startup distributes volume → 3PL executes

This is not volume sourcing.

It is volume routing.

The Only Viable Path: Protocol, Not Infrastructure

If Korean fulfillment startups cannot own demand, and cannot easily outcompete infrastructure-heavy players, then what can they own?

The answer is:

Protocol.

Specifically:

Inbound definitions

Inventory accuracy standards

Order state normalization

SLA enforcement

Packing rules

Return classification

Claim handling

Settlement logic

Warehouse performance scoring

This is the layer where the system actually breaks or holds.

And this is the only layer that can become defensible without owning:

traffic

warehouses

carriers

The real opportunity is not:

“We give you volume.”

It is:

“Without our protocol, this ecosystem cannot operate consistently.”

That is what a platform actually looks like in this structure.

Conclusion

Korea is structurally different.

Coupang has solved fulfillment through integration.

Naver is attempting to solve it through orchestration.

Startups operating within this system must decide:

Are they infrastructure?

Are they demand aggregators?

Or are they protocol layers?

Because only one of these is realistically defensible in Korea.

The mistake is to ask whether Korea has its own Deliverr.

The better question is:

In Korea’s fulfillment stack, who actually owns the protocol?