Who Pays for Free Shipping?

Naver's Quiet Bet on Korea's Logistics

Naver’s first-quarter call carried a few signals worth sitting with: membership-based unlimited free shipping, the conversion of core products into Naver Delivery, and the expansion of direct fulfillment contracts.

The easy reading is that this is Naver’s answer to Coupang’s Rocket WOW. I’d argue it’s something else. The real question Naver is wrestling with isn’t can we match Coupang on delivery. It’s the oldest question in commerce: where do you hide the cost of free shipping?

Because free shipping is never free. Someone always pays.

Two ways to absorb the cost

Coupang chose to internalize it. Fulfillment centers, camps, routing, last-mile density, returns, membership economics — all fused into one execution stack. For Coupang, free shipping isn’t a promotion. It’s a line in the operating system.

Naver took the opposite road. It doesn’t own a logistics network the way Coupang does. Instead it built the Naver Fulfillment Alliance — NFA — and grew Naver Delivery through partner 3PLs and parcel carriers. On paper, smart. Korea already has a dense bench of warehouse operators, fulfillment specialists, and carriers. Orchestrate that ecosystem through software, data, standards, and demand aggregation, and you get a competitive axis Coupang can’t easily copy — asset-light, fast, and capital-efficient.

So far, so good. My concern starts with one word: direct.

The hinge: direct contracts

I want to be precise about what we don’t know. Naver hasn’t disclosed how it prices NFA, how it allocates volume, how it settles with partners, or what operating obligations it imposes. So what follows is a structural reading, not a leak.

Here’s the structural shift. The moment Naver signs logistics contracts directly with sellers and pulls fulfillment costs and delivery fees into its own settlement layer, NFA’s character changes. It stops looking like an independent partner network and starts looking like an execution layer underwriting Naver’s membership economy.

And a 4,900 won monthly membership fee can’t fund unlimited free shipping on its own. If the shopper sees “free,” the cost moves somewhere they can’t see: into seller margins, product prices, NFA usage fees, parcel rates, or fulfillment spreads. The shopper stops paying. The system keeps paying.

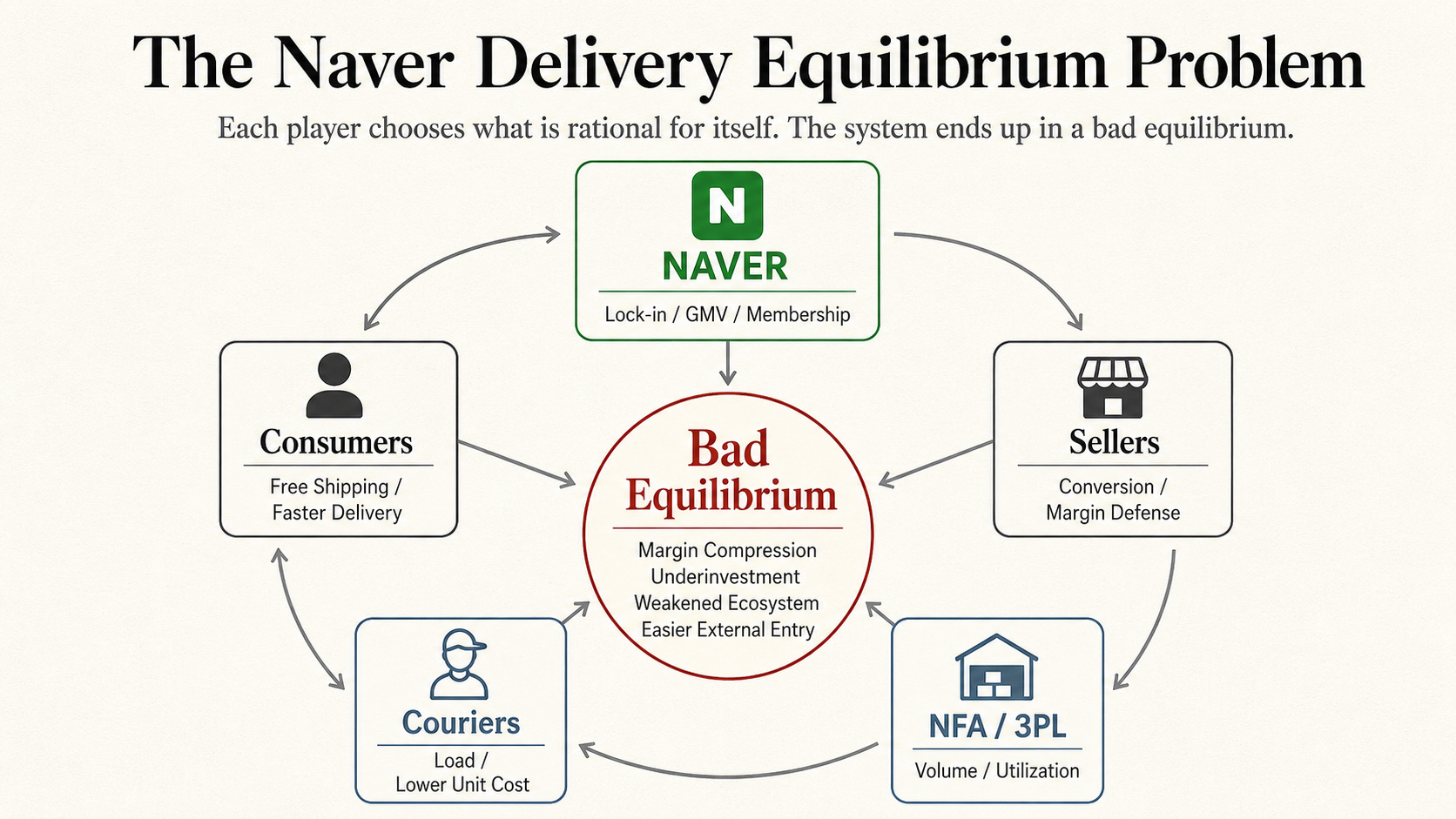

The bad equilibrium

When a platform that anchors one of Korea’s two dominant commerce poles pushes this model, sellers and logistics providers don’t opt in because the economics are good. They opt in because they need exposure, conversion, and volume to survive.

Short term, it looks like growth. Naver Plus memberships climb, Naver Delivery volume rises, commerce revenue prints well. NFA partners look like they’re winning — warehouses fill, sales rise. But the more a 3PL’s fixed costs depend on Naver volume, the more its bargaining power erodes. Past a certain threshold, contract rates and operating terms stop being negotiations. They become conditions of survival.

Every actor is rational on its own. Naver wants lower logistics cost to fund free shipping. Sellers need visibility. 3PLs accept thinner margins for volume. Carriers chase platform-scale shipments they can’t afford to lose. Add it up and the system drifts toward compressed margins, weaker investment capacity, and deeper platform dependency — a place that’s hard to back out of.

That matters most for the future, because modernization needs margin. Warehouse automation, AI-driven operations, robotic picking, smarter returns systems, merchant-facing logistics intelligence — none of it gets funded by a partner that’s busier but poorer. More work, more responsibility, less room to invest.

The honest counterargument

Here’s where a fair reader pushes back, and they’re not wrong to. Volume concentration can help. Higher utilization, fuller trucks, fewer empty miles — aggregation genuinely lowers unit cost, and some of that can flow back to partners as healthier margins rather than thinner ones. That’s the optimistic case for NFA, and it’s real.

The question is which force wins: the efficiency Naver’s orchestration creates, or the pricing leverage its volume hands it. Efficiency gains are shared only if the platform chooses to share them. Leverage gets exercised by default. That’s the part I’d want Naver to be deliberate about.

The Shopify mirror — read carefully

Shopify learned that owning and running logistics is far heavier than a software company expects, and walked much of it back. The lesson usually gets read as “don’t internalize logistics.”

But Naver’s position is the inverse, and that’s what makes it slippery. Naver isn’t acquiring carriers or taking on the full weight of ownership. It also isn’t simply leaving an independent ecosystem free to upgrade itself. It’s reaching for the third thing: economic control through volume, contracts, and settlement — control without ownership. That middle position is powerful precisely because it carries the upside of a logistics network without the balance-sheet weight. It’s also dangerous for the same reason — the party with the leverage isn’t the party carrying the risk.

What better looks like

If Naver genuinely wants to counter Coupang, partner margin is the wrong place to find the money for free shipping. Naver’s edge shouldn’t be acting as the prime contractor that absorbs logistics cost and redistributes it through platform power. Its edge should be the orchestration layer that lowers total system cost while making every participant better off.

Concretely, that’s not a slogan. It’s things like aggregating demand across sellers so carriers can raise trunk-line load factors instead of running half-empty routes; standardizing fulfillment data so 3PLs forecast labor and inventory more accurately; cutting failed deliveries and reprocessing returns more cheaply; consolidating shipments intelligently rather than just routing them. Lower total cost through better system design — not lower partner margin through stronger leverage.

The distinction is everything. The moment we stop asking who pays, free shipping stops being innovation and becomes a cost transfer inside the industry, dressed up as a consumer win.

The part that should worry Korea

If Naver’s strategy funds free shipping by draining the future investment capacity of Korea’s fulfillment and parcel ecosystem, then it isn’t only a play to slow Coupang. It risks pushing Korea’s logistics infrastructure into a weaker equilibrium.

And here’s the irony. A domestic logistics base hollowed out by margin pressure and underinvestment becomes easier for outside platforms to rent, squeeze, and integrate. Picture CJ Logistics, Hanjin, and Lotte competing hard for Naver volume while also absorbing low-margin cross-border parcels from AliExpress and Temu. That isn’t a path to a more advanced network. It’s a path to low-margin survival — and a survival-mode logistics sector is exactly the kind of infrastructure a Chinese platform would find convenient to build its own Korean execution stack on top of.

So Naver Delivery’s direct-contract strategy shouldn’t be filed under “one company’s commerce policy.” It’s an ecosystem question.

The real issue was never whether Naver can offer free shipping.

It’s whether Korea’s independent logistics infrastructure can survive the way Naver chooses to pay for it.